The Five Things to Know (and Never Forget) About Bear Markets

Introduction

A bear market is generally defined as a decline of 20% or more from recent market heights. Investors will feel pessimism and have a feeling of negativity related to their portfolio. When you read of bear markets in the financial press it is usually referring to a well known index such as the S&P 500. However, individual stocks can fall into this category as well if they are experiencing losses of 20% or more over a period of time.

The cause of bear markets are the result of a sluggish economy, rising interest rates, and inflation. Bear markets are a fact of investment life and should be expected over the lifelong journey of investing. According to investment data, a bear market happens about every 56 months.

Because the stock market usually has a downturn every five to seven years, most investors will experience several bear markets over their lifetime. In order not to be psychologically disturbed by these collapses in value, it is crucial for an investor to understand that downswings are normal and healthy aspects of investing—and even necessary sometimes.

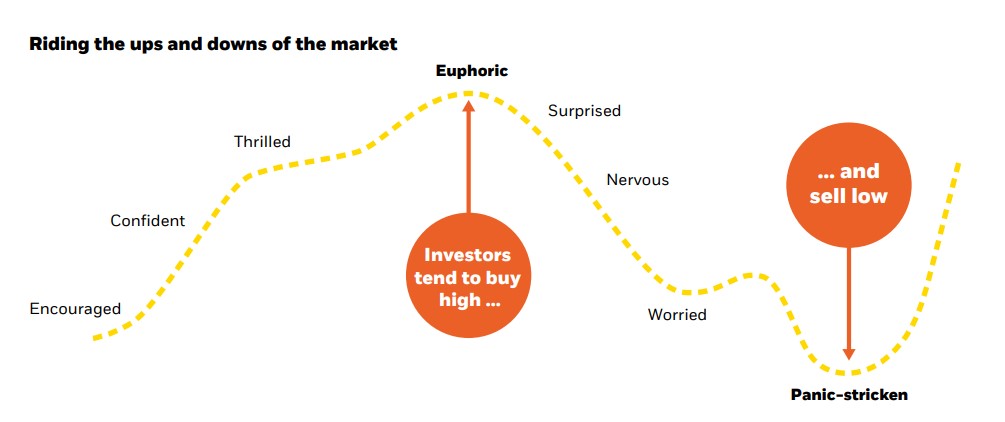

Having cognitive awareness of market cycles will help investors not to sell at the wrong time (selling when prices are relatively low) and buying back into the market at the wrong and inopportune time (when prices are relatively high).

This article will talk about Five Things That Every Investor Should Know (and Never Forget) About Bear Markets.

Bear Markets are Short-Lived

Most bear markets are short-lived. In fact, most of them last just a few months. The average bear market lasts just 289 days, according to data compiled by LPL Research. The longest bear market since 1928 was 630 days (about 21 months) which occurred in 1973-1974. The stock market lost about 48% in value during that period. (Seeking Alpha)

Bear Markets are Normal

Bear markets are a normal and an expected part of investing. Here is the challenge for all of us who invest in the market: ignore the news and financial media. We have said this countless times but it bears repeating. If we listen to the news, we might fall victim to Confirmation Bias—the tendency to favor information that confirms our preconceptions and ignore or discount facts that contradict them.

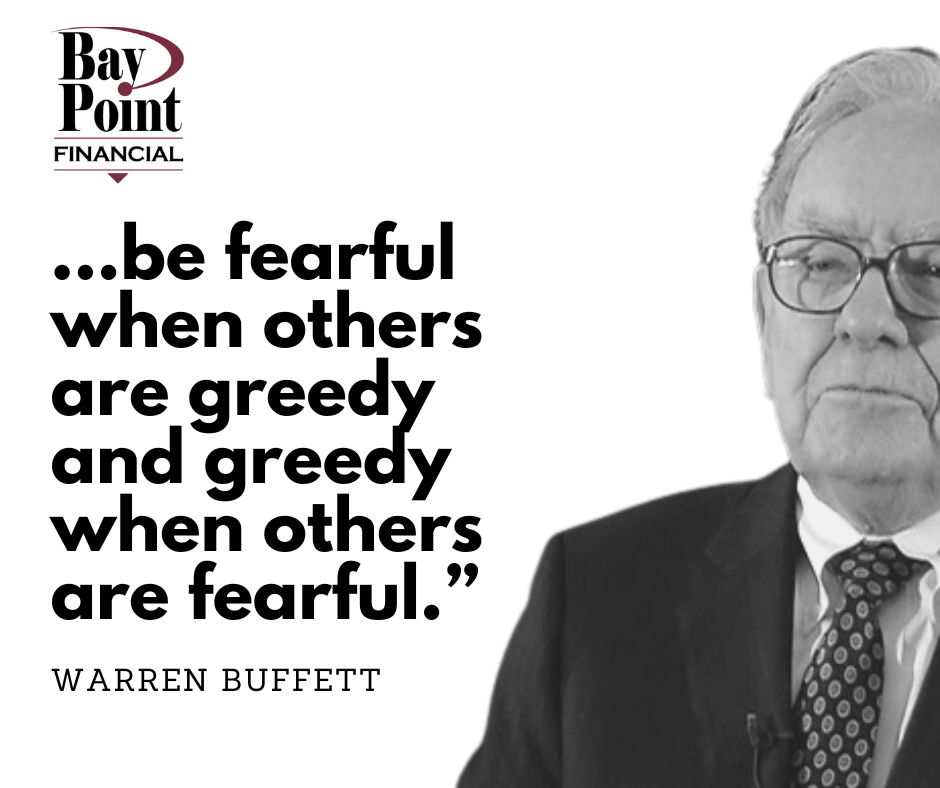

We may feel that the current market losses will NEVER end. We might feel that the losses will last forever and this leads us to become fearful. When we are fearful, we sell our investments at a loss. This is a mistake: as Warren Buffet says, “be greedy when others are fearful and be fearful when others are greedy”.

Bear Markets are Always Followed by Bull Markets

Of course bull markets are followed by bear markets. But, as simple as this truth is, it is often forgotten when an investor is in the midst of declining portfolio values and losses.

According to CFRA research there have been 14 bear markets since World War II (26 bear markets since 1929). What is interesting is that it took only 12 months for the market to find the bottom but the market losses were recovered within a 23 month period.

For example, since World War II, the U.S. stock market has experienced 13 bull-bear cycles, with the average bull market lasting 1,630 days and the average bear lasting 419 days (a decent return on investment for most investors). According to Investment News: “Over that period, the average bear market decline is 27%, while the average bull market gain is 167%. And the average recovery time from a bear market is 26 months.”

Markets are Positive a Majority of the Time

The stock market on the whole is up more than down. When looking at the S&P 500 Index going back to 1926, the index had a positive calendar year return over 60% of the time. The 20-year annualized return is close to 10% (9.52%). Investors who stay the course are rewarded with positive returns and the opportunity to create wealth.

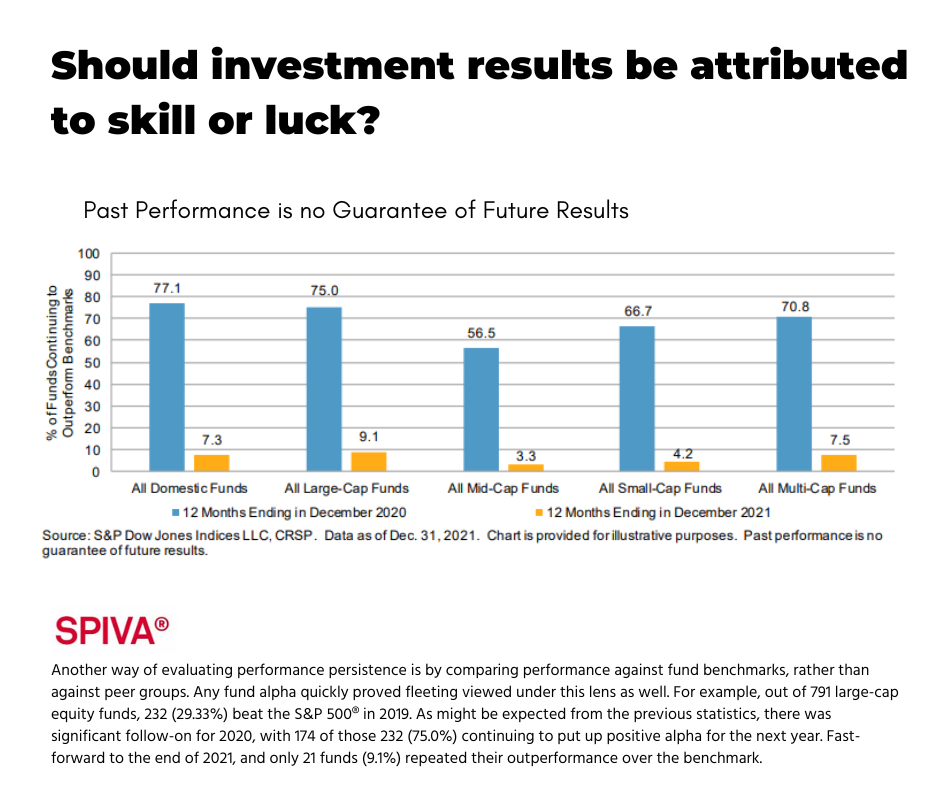

Ignore Active Management

Beware that when markets are volatile and bearish, many experts will make the claim that this is the time that active management "shines." The idea (and the claim) is that when markets are in a free fall, active managers can exploit the bad times by finding mispriced stocks and markets.

One only has to review the SPIVA study that looks at the data of active managers and compares their performance to a simple index strategy like the S&P 500. Their findings? SPIVA writes: "[...] shows that regardless of asset class or style focus, active management outperformance is typically short-lived, with few funds consistently outranking their peers or benchmarks." Active management simply doesn't work and fails to deliver market returns due to transaction costs and the buying and selling of individual securities at the wrong time.

Conclusion

Remember that bear markets are a normal part of investing. They’re not something to fear but rather an opportunity to understand and manage your portfolio so it continues growing even when the market takes its dips (like always will)

Sources:

https://www.investmentnews.com/galleries/dont-panic-thereve-been-13-bull-and-bear-markets-since-wwii